seed-round

Investor data room

Startup Traction

Investor Pitch

Fundraising

Financing Option

Should You Bootstrap or Raise Capital? The Decision Framework That Actually Works

Adhrita Nowrin

Apr 6, 2026

Most bootstrap-vs-raise advice on the internet boils down to "it depends on your goals." That is not a framework. And honestly, we are all tired of hearing it.

We work with pre-seed to pre IPO founders across the UK, US, and UAE. The ones who get this decision wrong do not fail because they picked the wrong path. They fail because they picked without doing the math of what the decision costs. So here is the actual math, the actual trade-offs, and a framework that forces an honest answer, one that we use internally at askRIA while onboarding founders.

Bootstrapping vs Raising Capital: The Real Cost (With Numbers)

Before the framework, founders need to understand what each option actually costs. Not in theory. But the impact on the cap table over successive rounds.

The dilution math most founders skip:

A two-founder team starts with 100% ownership. Before any external raise, a typical pre-seed company carves out 10% for an employee stock option pool (ESOP) and 1-2% for advisors. That puts combined founder ownership at 88-89% before a single investor writes a cheque.

Now the raises begin.

According to Carta, Flowjam, and Rebel Fund data from 2025, here is what a realistic dilution trajectory looks like for a UK or US software startup:

Pre-seed: Raise £500K on a £5M post-money valuation. Founders give up 10%. Combined founder ownership drops to ~79%.

Seed: Raise £2M on a £10M post-money valuation. Founders give up 20%. The ESOP gets topped up to 15%. Combined founder ownership drops to ~58%.

Series A: Raise £8M on a £40M pre-money valuation. Founders give up another 17%. ESOP expanded to 18%. Combined founder ownership drops to ~42%.

Three rounds in. The founders built the company, found product-market fit, hired the team, and closed the customers. They own 42%.

That is not a bad outcome if the company is worth £48M. 42% of £48M is £20M. But it is a very different outcome from 100% of a £3M bootstrapped company, which is £3M.

The question is not "which percentage is better." It is "which total value is bigger, and how confident am I in reaching it?"

The bootstrapping cost most founders ignore

Bootstrapping is not free. It costs time, personal savings, and opportunity.

A typical early-stage founder in the UK burns through £3,000-5,000 per month in personal living costs while building. Add a co-founder, a contractor, basic infrastructure (cloud, legal entity, accounting), and the real monthly burn for a two-person bootstrapped startup sits around £8,000-12,000. That is £96,000-144,000 per year before any customer acquisition spend.

Most bootstrapped SaaS companies take 12-18 months to reach £5K MRR. During that time, the founders are effectively paying to work. If personal savings run out at month 10, the startup dies regardless of how good the product is.

ChartMogul's 2024 SaaS Growth Report found that bootstrapped SaaS companies report a median annual growth rate of 23%. VC-backed companies grow faster in absolute terms, but bootstrapped ones adapted more quickly when the market slowed in 2022-2023. The constraint forced sharper decisions about what to build and who to sell to.

The 6-Factor Decision Framework

1. What is the competitive clock?

If the market is winner-takes-most (AI infrastructure, fintech payments, marketplace plays), a funded competitor will outrun a bootstrapped one. In Q2 2025, AI startups captured 28% of all global VC funding, roughly $19 billion in a single quarter, according to Crunchbase data. A founder bootstrapping in that space is bringing a spreadsheet to a gunfight.

If the market is vertical SaaS, niche B2B, or professional services, the clock is slower. Bootstrapping buys iteration time without board pressure.

Test: If a competitor raised £5M tomorrow, would it make the bootstrapped path unviable within 12 months?

2. What are the actual 18-month costs?

Not the optimistic number. The real one. Founders routinely underestimate by 40-60%.

Build a line-item budget: salaries (or founder living costs), ESOP administration, legal (incorporation, SEIS/EIS compliance if UK, IP assignment), cloud infrastructure, accounting, insurance, customer acquisition, and three months of buffer runway. That buffer matters because fundraising itself takes 4-6 months on average, according to DocSend data, and founders need cash to survive the process.

In the US, the median seed round is $2.5-3.5M. In Europe, £1-2M. In the UK specifically, seed deals made up 32% of all VC term sheets in 2024, more than double their 2021 share, per PitchBook. But 78% of startups are still self-funded initially, per Crunchbase. The question is not whether to bootstrap at all. It is when to stop.

Test: Write down the 18-month number. Add 40%. Can personal funds and projected revenue cover it?

3. What is the dilution tolerance?

This requires modelling, not vibes. And caffeine.

Build a simple cap table model with three scenarios: (a) raise pre-seed only, (b) raise pre-seed + seed, (c) raise pre-seed + seed + Series A. For each, plug in realistic round sizes and valuations for the sector. Calculate combined founder ownership at each stage.

The median pre-seed dilution in the US is roughly 19.7%, according to Flowjam's 2025 analysis. In Europe, it is about 21%. Seed dilution runs 20-25%. By Series A, founders typically hold 40-55% combined, according to Sesamers' startup equity data.

Most VC investors expect founding teams to hold at least 50% equity after a Series A, per J.P. Morgan's cap table management guidance. Below that, founder incentive drops and the company becomes harder to fund in subsequent rounds.

Test: Model the cap table through three rounds. Is the founder comfortable with the resulting ownership at a realistic exit valuation?

4. Is there product-market fit, or the hope of it?

Ten beta users is not product-market fit. Three paying customers is not product-market fit. (We know because we have told ourselves both of those stories.)

Product-market fit is measurable: low churn, organic referrals, customers pulling the product out of the founder's hands. If it is not there yet, raising capital will not create it. It will just let the founder burn cash faster while searching.

Founders who bootstrap to early traction and then raise get significantly better terms. Atlassian bootstrapped for eight years before raising. Mailchimp sold for $12 billion without taking VC money. Calendly bootstrapped to a $3 billion valuation before outside investment. These are outliers, but the principle is consistent: proven traction converts to lower dilution and better investor quality.

Test: Is there measurable retention and organic growth? Or is the raise funding the search for those things?

5. What does the business model demand?

Some models require capital before revenue is possible. Hardware with manufacturing costs. Biotech with clinical trials. Marketplaces with liquidity problems. These cannot bootstrap past a point. The unit economics demand outside money.

Other models generate cash early. Consulting-to-product plays. Vertical SaaS with low infrastructure costs. API tools. Content businesses. These can self-fund for longer, and doing so means raising later at higher valuations.

Test: Does the model generate revenue before it needs scale capital? Or does it need capital to generate any revenue at all?

6. Is the investor network real or theoretical?

Only about 0.05% of startups raise VC funding. Seed fundraises take 4-6 months on average. Founders typically connect with 100-200 investors before closing a seed round. DocSend's research shows 37% of successful founders close a seed round in 1-6 weeks, but 31% take 19 weeks or more.

If a founder does not have warm introductions to investors who understand the market, the fundraise will take the longer end of that range. That is 4-6 months not building product, not talking to customers, not iterating. Sometimes the better use of those months is bootstrapping to metrics that make the fundraise shorter next time.

Test: Are there 10+ warm investor relationships ready to activate? Or would this be a cold-outreach fundraise?

The Hybrid Path: Why "Bootstrap Then Raise" Wins the Math

The data supports a specific pattern: bootstrap to validate, then raise to scale.

A founder spends 6-12 months self-funding. Gets to £5-10K MRR. Proves unit economics. Then raises a pre-seed or seed round with real numbers.

The terms are measurably better. A startup with £10K MRR raising at a £8-10M valuation gives up less equity than a pre-revenue startup raising at a £3-5M valuation for the same amount of capital. The dilution difference compounds across every subsequent round.

Bootstrapped startups also maintain a five-year survival rate of 35-40%, compared to 10-15% for VC-backed companies, according to Jumpstart Magazine's analysis. And 25-30% of bootstrapped startups reach profitability early, versus 5-10% of funded ones. Constraint is not just a mindset. It is a survival mechanism.

Where the Decision Meets Execution: The Fundraising Process

Here is where most guides stop. "Make your choice and go." That is incomplete. Because the decision to raise creates a second problem: execution.

A seed fundraise is a full-time job running parallel to building the company. The founder needs a structured data room, clean financials, an organised cap table, legal documentation, and the ability to manage 30-50 investor conversations with different timelines, different information requests, and different levels of engagement.

Most founders run this process from a Google Drive folder. Scattered PDFs. No version control. No visibility into which investors opened which documents. No idea what is missing until an investor asks for it mid-diligence and the deal stalls for a week while the founder scrambles.

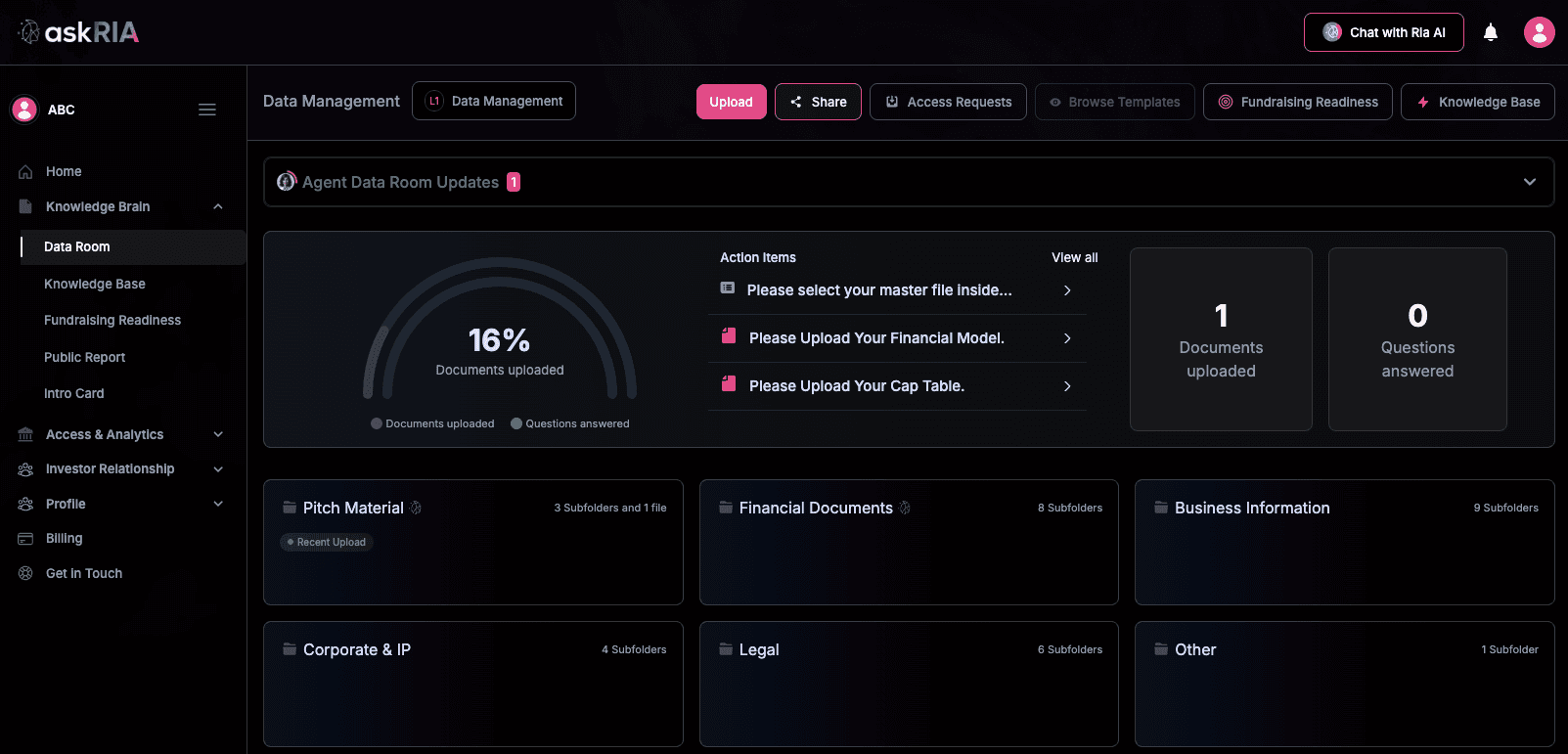

This is the problem we built askRIA's Fundraising Agent to solve.

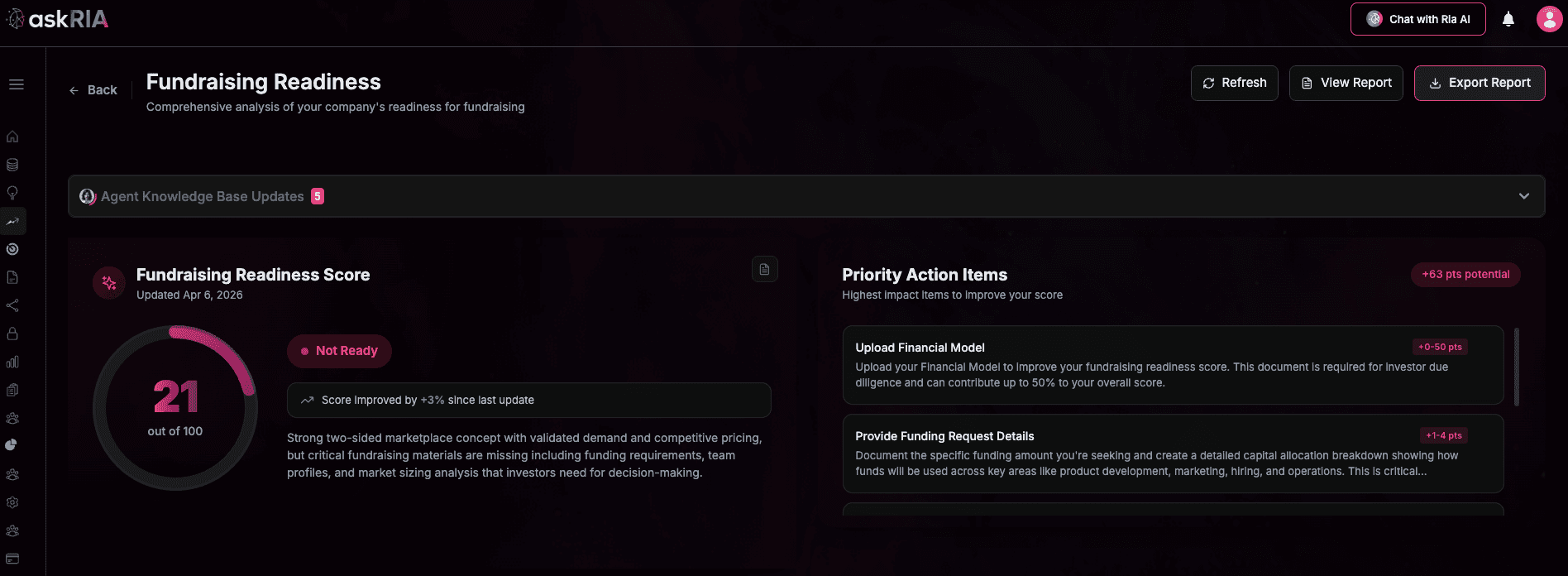

When a founder uploads documents to askRIA, the platform automatically structures a data room. It identifies which documents are missing. It scores the company's investor readiness with an Investor Readiness Score, flagging gaps in the cap table, financials, and legal documentation before investors see any of it.

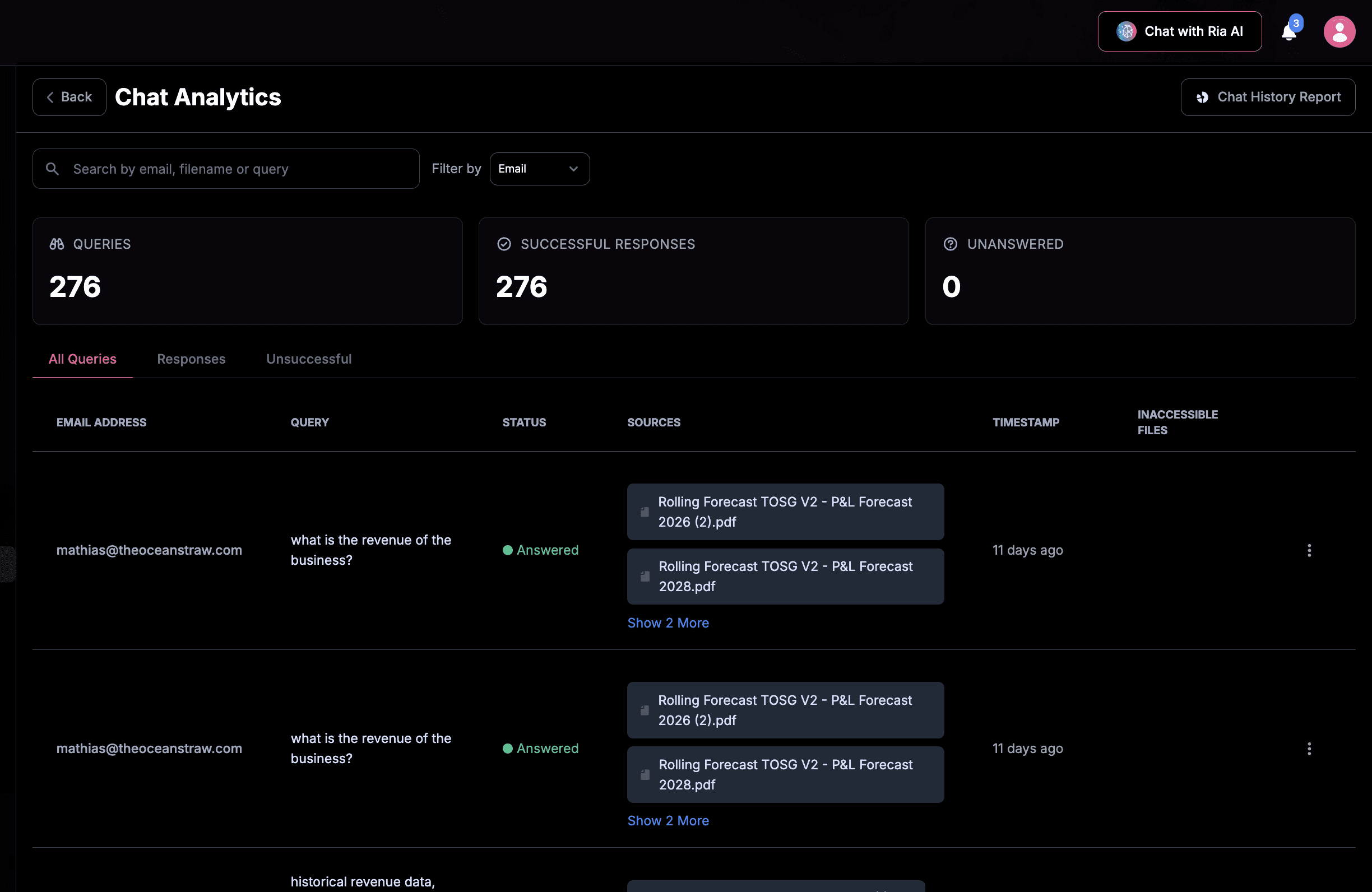

The founder-side agent then tracks engagement: which investors viewed which documents, how long they spent, which questions remain unanswered. That data turns a guessing game into a pipeline. A founder who knows Investor A spent 22 minutes in the financials but has not opened the cap table can follow up with precision instead of a generic "just checking in" email.

Most founders underestimate how critical this step is, if you’re not sure what a “structured” data room actually looks like, here’s a link to the breakdown of the data room set up.

What investors see on the other side

When a founder shares an askRIA data room, the investor experience is fundamentally different from receiving a Dropbox link.

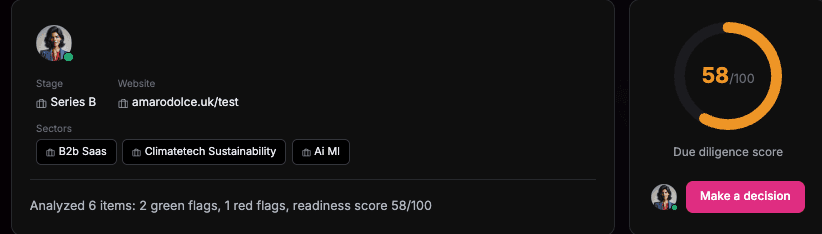

askRIA automatically extracts 100+ due diligence questions from the uploaded documents. Each answer is scored. Red flags and green flags are surfaced without manual review. The deal is scored against the investor's custom investment thesis and criteria.

This happens automatically. No junior analyst spending three days building a diligence spreadsheet from scratch. The investor opens the data room, and the structured evaluation is already there.

Why does this matter to founders?

Because the average funding round takes about 115 days to close, per Phoenix Strategy Group. Anything that compresses the investor's evaluation time compresses the overall timeline. Founders who make the investor's job faster get term sheets faster, because time is money and the easier a founder makes it for the investor, the faster the decision is made.

A bootstrapped founder who decides to raise in month 9 can go from documents uploaded to a structured-data-room shared to 100+ investors, in 24hrs by building their data room on askRIA.

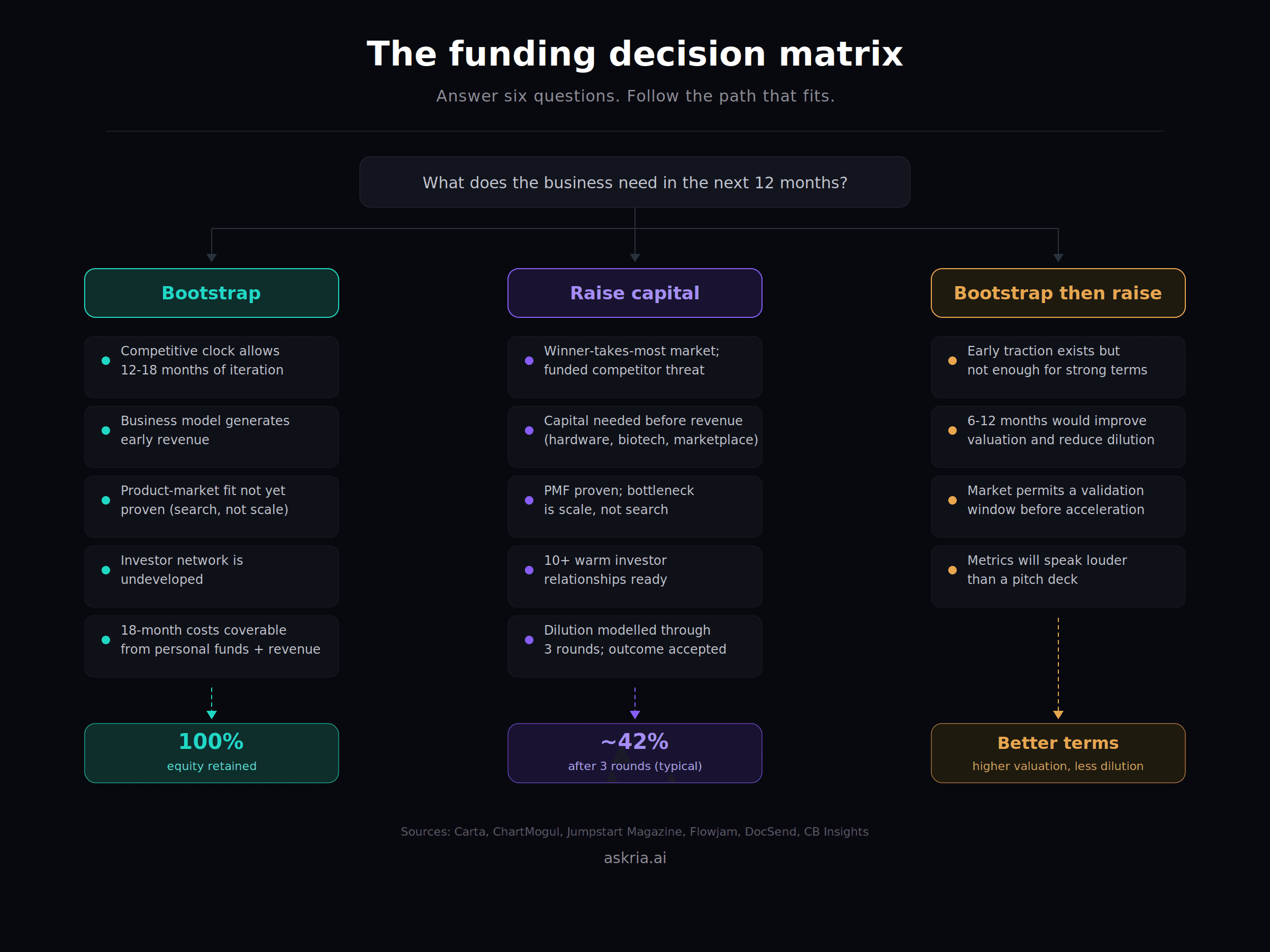

Bootstrap if:

Competitive clock allows 12-18 months of self-funded iteration

Business model generates early revenue

Product-market fit is not yet proven (raising pre-PMF is raising to search, not to scale)

Investor network is undeveloped

18-month costs are coverable from personal funds and revenue

Raise if:

Market is winner-takes-most and a funded competitor would make bootstrapping unviable

Business model requires capital before revenue (hardware, biotech, marketplace)

Product-market fit is proven and the bottleneck is scale, not search

10+ warm investor relationships are ready to activate

Founder has modelled dilution through three rounds and is comfortable with the outcome

Bootstrap then raise if:

Early traction exists but is not enough for strong raise terms

6-12 months of self-funded growth would meaningfully improve valuation and reduce dilution

The market permits a validation window before needing to accelerate

Metrics will speak louder than a pitch deck

The Numbers That Matter

Survival: Bootstrapped startups have a 35-40% five-year survival rate vs 10-15% for VC-backed (Jumpstart Magazine). Bootstrapped startups also show a 38% ten-year survival rate vs 20% for funded ones.

Growth: VC-backed SaaS grows 100%+ faster than bootstrapped in early stages (SaaS Capital). Bootstrapped SaaS has a median 23% annual growth rate (ChartMogul).

Profitability: 25-30% of bootstrapped startups reach early profitability vs 5-10% of funded companies (Jumpstart Magazine).

Fundraising reality: 0.05% of startups raise VC. Average round takes 115 days to close. Founders connect with 100-200 investors before closing a seed. 60% of pre-Series A companies fail to reach Series A.

Dilution benchmarks: Pre-seed: 10-15%. Seed: 20-25%. Series A: 15-25%. Cumulative founder ownership post-Series A: typically 40-55%.

FAQs

What is bootstrapping vs raising capital? Bootstrapping means funding a startup through personal savings, revenue, and internal cash flow without giving up equity. Raising capital means selling equity to outside investors (angels, VCs, accelerators) in exchange for funding. Both are financing tools with different cost structures: bootstrapping costs time and personal capital; raising costs ownership and control.

How much equity do founders lose per funding round? At pre-seed, 10-15%. At seed, 20-25%. At Series A, 15-25%. After three rounds with ESOP allocations, two co-founders who started at 100% typically hold 40-55% combined. The exact numbers depend on round size, valuation, and ESOP expansion at each stage.

Can founders bootstrap first and raise later? Yes, and the data suggests this often produces better outcomes. Founders who reach £5-10K MRR before raising can command higher valuations, give up less equity, and attract investors with stronger track records. Atlassian bootstrapped for eight years. Calendly bootstrapped to a $3B valuation. Mailchimp exited at $12B with no VC funding.

How long does a seed fundraise actually take? On average, about 4-6 months from first pitch to money in the bank. DocSend data shows 37% of successful founders close in 1-6 weeks, 32% take 7-18 weeks, and 31% take 19+ weeks. First-time founders should budget 6 months and plan runway accordingly.

What is the average seed round size in 2025-2026? US median is $2.5-3.5M (Carta). European seed rounds are typically €1-2.5M (Pitchwise). AI startups command a premium at $4.6M median deal size (CB Insights). UK seed deals made up 32% of all VC term sheets in 2024 (PitchBook).

What is a data room and why does it matter for fundraising? A data room is a structured collection of a company's documents shared with investors during due diligence: financials, cap table, legal agreements, pitch materials, and supporting data. A disorganised data room slows investor evaluation and kills deal momentum. askRIA automatically structures data rooms from uploaded documents, identifies missing items, scores investor readiness, and tracks which investors engage with which documents.

What is investor readiness and how is it measured? Investor readiness measures whether a company's documentation, financials, and legal structure are complete enough to survive investor due diligence without delays. askRIA generates an Investor Readiness Score that flags missing documents, red flags in financials and cap table structure, and documentation gaps, so founders can fix issues before investors see them.